Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

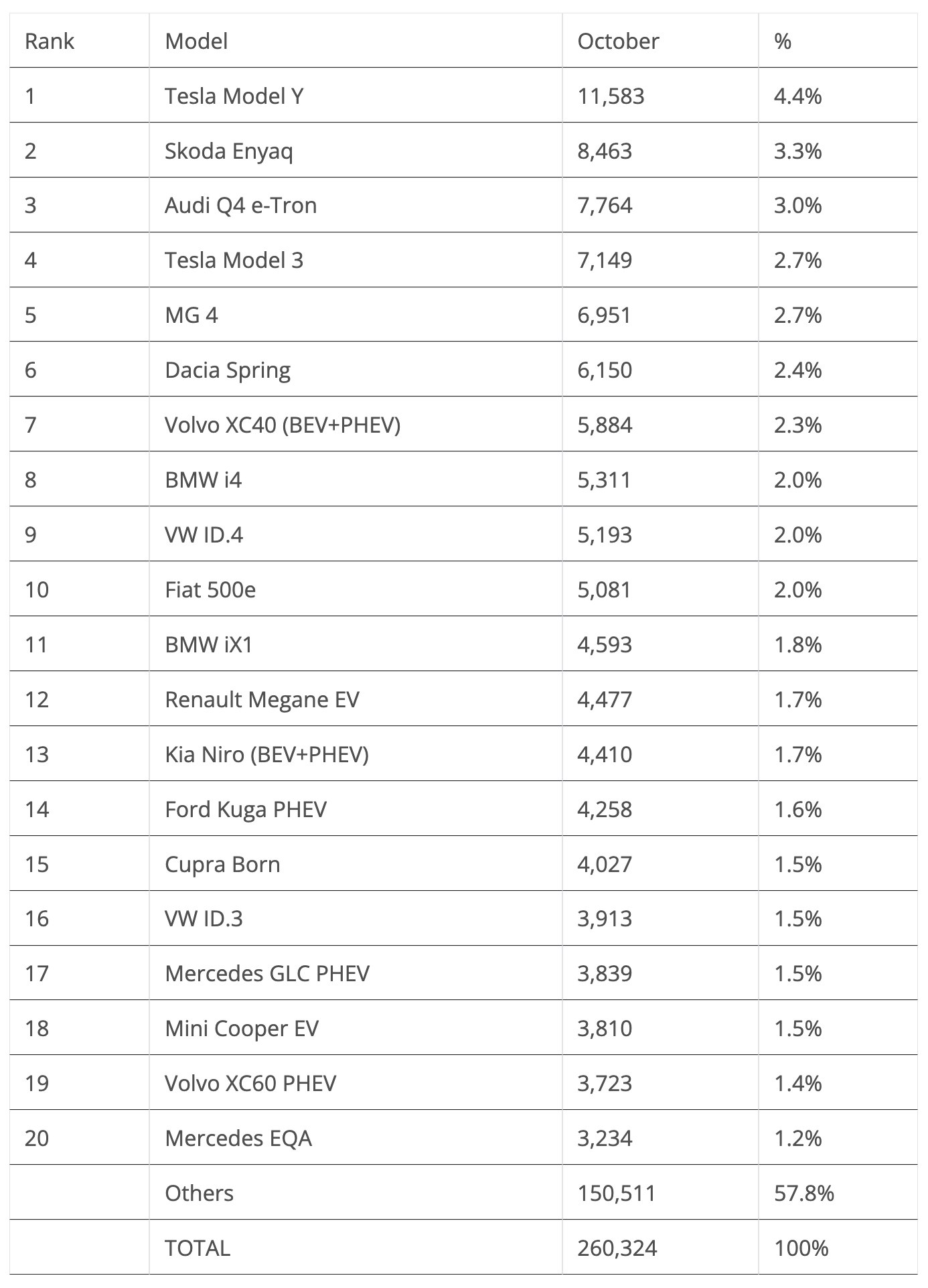

Approximately 260,000 plugin vehicles were registered in October in Europe, +24% year over year (YoY). The overall market also grew by double digits, +14%, but this result was still down 15% on October 2019, the last normal month on the market.

Last month’s plugin vehicle share of the overall European auto market was 25% (16% full electrics/BEVs). With that result, the 2023 plugin vehicle share remained at 23% (16% for BEVs alone).

Most of the plugin vehicle growth came from BEVs, which were up 39% YoY, while PHEVs were up by just 3%. Pure electrics accounted for 65% of all plugin sales in October, against a 2023 average of 67%.

The highlights of the month were the #2 Skoda Enyaq and #3 Audi Q4 e-tron, which had record results, compensating for the Volkswagen ID models’ absence from the top spots. But let’s look closer at October’s plugin top 5:

#1 Tesla Model Y — For the 12th month in a row(!), Tesla’s crossover was the best selling EV in Europe, and with no other model breaking into five-digit performances, one cannot really imagine who or what could break the Model Y’s domination in Europe. In October, the midsizer had 11,583 registrations. However, this year could be considered “Peak Model Y” in Europe. The midsized crossover should continue to post similar results in the coming quarters in Europe, but do not expect sales to increase significantly over current volumes, as I am confident the Model Y has already reached the market’s natural limits. After all, the Model Y, an expensive midsize model, is already Europe’s best selling model in the overall market…. Also limiting its growth will be the refreshed Tesla Model 3, which could steal some sales from it, even if Europeans aren’t really into sedans these days. Regarding last month’s performance, the Model Y’s biggest European markets included the UK (1,905 units), France (1,833 units), Germany (1,649 units), Belgium (673 units), and other countries at significantly lower volumes.

#2 Skoda Enyaq — The Czech crossover is a sure value in the EV arena, and has even managed to score a record month in October, with the good looking crossover ending the month with a podium presence thanks to 8,463 sales. Expect sales to continue strong in the coming months, especially now that production constraints have finally ended. Regarding the Enyaq’s October results, its biggest market was Germany (2,579 registrations), followed at a distance by Sweden (808 registrations) and Switzerland (628 units).

#3 Audi Q4 e-tron — Audi’s compact crossover won a podium presence in October thanks to 7,764 registrations, a new record for the premium compact crossover. With increased production availability, the Audi EV is now only dependent on demand to improve its performances. Regarding the Q4’s October performance, its main market was the UK (1,960 registrations), followed by its domestic market of Germany (1,867 registrations) and then at a distance by Belgium (778 registrations), a known stronghold for the four-rings brand.

#4 Tesla Model 3 — This was the first month that the refreshed sedan was delivered in Europe, and one can say that it got off to a good start, scoring 7,149 units in October. The US sedan is expected to have a strong end of the year, with the Model 3 possibly even breaking its sibling’s domination at the top of the ranking in December when the Toyota-fied sedan is expected to have an above-average “high tide.” Looking at October’s performance, Germany (1,607 registrations) was its biggest market, followed by France (1,353 registrations) and the UK (753 registrations).

#5 MG4 — The dragon slayer hatchback is fulfilling SAIC’s best expectations, with another top 5 presence thanks to 6,951 registrations. With almost unbeatable value for money, and the small detail of being 10,000 euros cheaper than its most direct competition (the VW ID.3 and Renault Megane EV), the Sino-British model is becoming the reference point in Europe’s compact hatchback class. This category used to be the sheer definition of what a European car was, with examples like the VW Golf, Skoda Octavia, and Opel Astra. Regarding the MG4’s October performance, this time its main market was not the UK (1,497 registrations), with higher volumes delivered in France (1,864 registrations) and Germany (1,722 registrations). Talk about winning in the opponent’s field….

Looking at the rest of the October table, we should highlight the year-best result of the #6 Dacia Spring, 6,150 registrations. With the end of subsidies for Chinese EVs in France coming soon, expect the Sino-Romanian to continue posting strong results through the year end.

The BMW i4 also hit a year best result, 5,311 registrations — the prime example of the BMW Group’s strong results in October. In addition, the #11 BMW iX1 posted a positive 4,593 registrations, the veteran Mini Cooper EV had a year-best score, 3,810 registrations, and down below, we are starting to see the recently introduced BMW i5 ramping up fast, having reached 1,029 units this month. Sure, this is still far from the 2,702 units of the full size leader Audi Q8 e-tron, but I would not be surprised if in some six months, the good looking Beemer (a rarity, these days…) started breathing on the back of the big fat Audi.

Still on the topic of the full size category, we should highlight that the best selling model in October was not the Audi Q8 e-tron, but its Volkswagen Group stablemate, the Porsche Cayenne PHEV. Thanks to a deep refresh, including a new 26 kWh battery, the sports SUV (one of the few models where such a moniker actually makes sense) reached record heights. It scored 2,979 registrations, thus allowing it to beat the Audi SUV, the current category leader.

In October, the best selling plugin hybrid model was the Ford Kuga PHEV, which ended in #14, followed by the Mercedes GLC PHEV in #17 and the Volvo XC60 PHEV in #19. Expect the German SUV to be a strong contender for the category title next year.

Below the top 20, besides the previously mentioned models, we should also highlight the Peugeot 308, which had a record 2,227 registrations, a new record. Although, intriguingly, only 150 units belonged to the BEV version….

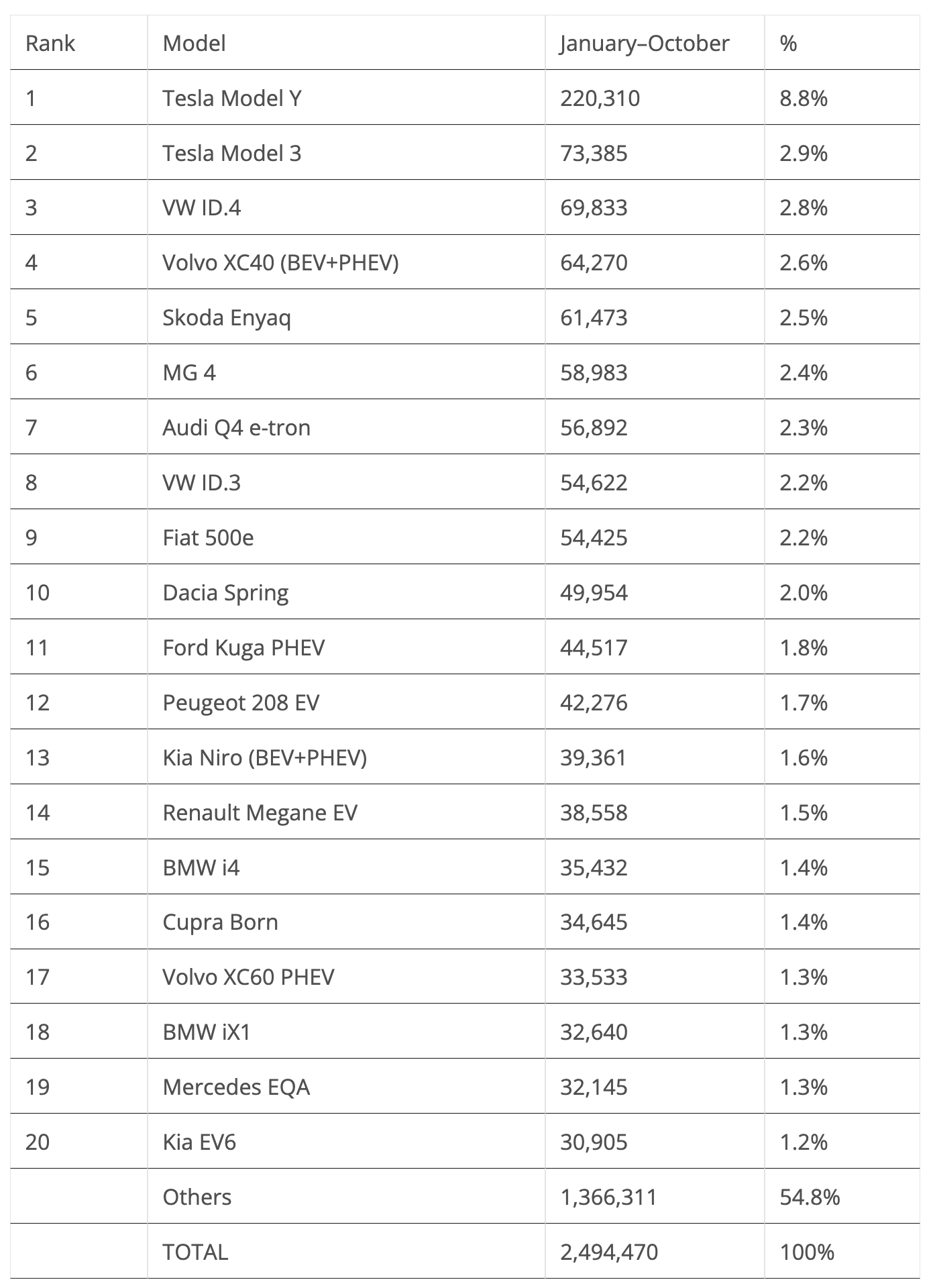

Looking at the 2023 ranking, with the Tesla Model Y having three times as many deliveries as the runner-up Tesla Model 3, the attention is now focused on the remaining podium positions.

But even there, it seems the decisions are already made. The VW ID.4 doesn’t seem able to compete for the runner-up spot, especially considering recent demand issues on the part of the German crossover, as well as the fact that the Model 3 should have a BIG December.

If the podium standings end as they currently are, then the 2023 podium will be exactly the same as the 2022 edition.

On the other hand, regarding the #4 Volvo XC40, its position isn’t yet safe, as the #5 Skoda Enyaq is quickly closing in on the Belgian-built Swede. We might have a surprise here towards the end of the year.

Audi’s Q4 e-tron was the Climber of the Month, jumping to 7th position, surpassing the VW ID.3 in the process. The ID.3 was once seen as the future successor of the VW Golf, born to lead the European market. Oh, how those days are gone….

The remaining position changes came in the second half of the table, with the BMW i4 climbing to #15 at the cost of the Cupra Born and the BMW iX1 joining the table in #18, confirming the crossover’s popularity.

In the auto brand ranking, Tesla is leading with a comfortable 12.1% share of the plugin market, but it has seen its share drop in October by 0.6% share. We shouldn’t read too much into this, as it is the first month of the quarter. Most likely, Tesla will recover the lost share in the next two months.

On the other hand, Volkswagen keeps on losing share. It is now down to 8.2%, dropping 0.2% compared to the previous month due to a slow month from its ID.3 and ID.4 best sellers. The German brand has lost 0.5% share in just two months. Does this mean that something is rotten in the Kingdom of Volkswagen?

Profiting from Volkswagen’s woes, rising BMW (8.2%, up 0.1%) surpassed the Wolfsburg make, with the Bavarian now the new runner-up. This means that the 2023 podium is now replicating 2022’s final standing.

And it could be worse still for Volkswagen, because #4 Mercedes (7.7%, up from 7.6%) is also on the rise, and with only 0.5% share separating these two, we might even see the German brand being kicked off of the podium!

But while the Volkswagen brand is bleeding, its premium cousin, Audi, is on the way up. After a significant rise from 5.4% share to 5.6% in October, the Ingolstadt make has surpassed Volvo (5.6%) and is now 5th, some 600 units ahead of the Swedish brand.

Arranging things by automotive group, despite the namesake’s brand drop, Volkswagen Group was up to 20.6%, from 20.2% in September. That is thanks to brilliant performances across the board: from Porsche (Cayenne PHEV record score) to Skoda (Enyaq record score), passing by Audi (Audi Q4 record) and Cupra. This, added to a slight drop from runner-up Stellantis (13.9%, down from 14% in October), allowed the German conglomerate to increase its lead even further.

This raises a significant question: If all the remaining brands from the VW galaxy are rising, why is Volkswagen dropping? Do not blame it just on the MEB platform and high costs, because the other brands are profiting from it. In my point of view, it is the design and how the ID models are being marketed. While one knows what a Skoda Enyaq is and stands for (practicality and value for money), and the same for the Cupra Born (Golf GTI for the electric era) and the Audi Q4 e-tron (a compact version of the Audi Premium-ness bratwurst), the VW ID.3 & 4 are … too middle of the road. And while that could be compensated for with competitive pricing, because their prices are average, at best, Volkswagen is watching its buyers go elsewhere.

Back to the top 5 OEMs, #3 Tesla was down to 12.1%, while off the podium, #4 BMW Group was up to 9.8%. We have a new #5 in the form of Hyundai–Kia. This is the third position change in a row happening in the 5th spot. Previously, in August, Hyundai–Kia removed Geely–Volvo from the top 5. Then, Mercedes Group removed the Korean OEMs from the last position on the table in September. Now, Hyundai–Kia (8.4%) has recovered the 5th position, thanks to a slow month from the Mercedes-Benz Group (8.3%), hurt by the current transition happening in the Smart brand.

Finally, we have some good news for #7 Geely–Volvo: its market share is finally recovering, going up by 0.2% to 8%.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

CleanTechnica Holiday Wish Book

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.