Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

A closer look at the best-selling automotive groups for plugin vehicles — part 2 of 4.

This is the second edition of a look into the top EV-selling OEMs. To have a look at the first edition, please check it out here. In this second one, we have a look at Hyundai–Kia, Toyota, GAC, and Mercedes.

For more information on these OEMs, don’t forget to check out our report on the top 20 EV brands and auto groups in the world.

Hyundai–Kia

Hyundai Motor Company, as it is officially known, is a South Korean automotive group based in Seoul.

It was founded in 1967 and currently it is the full owner of the namesake brand (Hyundai) and the luxury brand Genesis, while being the largest shareholder (34%) in former rival Kia — since Kia declared bankruptcy in 1997, during the Asian financial crisis.

While Kia is formally part of the Hyundai group, because it isn’t fully owned by Hyundai, that means that Kia retains a certain degree of autonomy. So, while the Hyundai–Kia association isn’t an Alliance of Equals, like the Renault–Nissan–Mitsubishi Alliance, Kia’s status isn’t as limited as, say, Audi, within Volkswagen Group.

Hence why on the sales articles I call them Hyundai–Kia.

Within the three brands, Kia is the best selling one, with 51% of the OEM’s sales. It is closely followed by Hyundai, with about 47% of the OEM’s sales. Niche Genesis is responsible for the remaining 2%.

Looking at individual models, the OEM has a balanced lineup, with the top sellers being the retro-futuristic Hyundai Ioniq 5, representing 19% of the OEM’s EV sales this year, and its sportier cousin, the Kia EV6, is second, with 13% of sales. Those two are followed closely by the Kia Niro (BEV+PHEV) and Hyundai Kona EV, with 12% of sales each.

With several new models landing or in ramp-up stage (Kia EV3 & Kia EV5, Hyundai Inster/Casper EV, & Hyundai Ioniq 9), expect the Korean OEM to continue growing steadily in 2025, probably reaching the break-even point in its EV business as a consequence.

When it comes to China, the fact that its operations there are minimal — they represent just 1% of all of the OEM’s plugin sales, and counting all powertrains sales, they move fewer than 250,000 units a year, or 6% of total Hyundai–Kia sales — will eventually serve as an advantage to the Koreans. It means that if they eventually leave China, their sales and production output will not be seriously affected.

Something that other legacy OEMs cannot say….

Toyota

It feels a bit strange to treat Toyota as a middle-of-the-pack OEM, but that is the current reality of the Japanese make when it comes to plugins.

Toyota is the biggest Japanese carmaker (and the largest in the world). Based in the Aichi prefecture, it started making vehicles in 1936, and it is a familiar name worldwide. The Toyota OEM has a few brands under its umbrella:

- Toyota itself

- Lexus — luxury arm of Toyota

- Daihatsu — brand focused on city and kei cars, but also offers a few compact MPVs and crossovers

- Hino — commercial vehicle maker.

Besides these fully-owned brands, Toyota is also the largest shareholder of Subaru (20%) and part of a couple of joint ventures (JV) in China, like FAW–Toyota and GAC–Toyota, where it holds 50% of them.

FAW–Toyota makes the China-only Toyota bZ3 sedan, while GAC–Toyota makes the local Toyota bZ4X.

In this case, we will be focusing on the namesake brand, which is by far the best-selling plugin make in the group, representing 80% of sales.

Unlike what some might believe, Toyota’s sales aren’t that PHEV-heavy, as 44% of Toyota’s total plugin sales are actually coming from pure electrics, and two out of the three best-selling models are BEVs. The bZ4X SUV is responsible for 24% of its plugin sales, while the China-only bZ3 sedan amounts to 19% of deliveries.

Still, the best-selling Toyota plugin is a PHEV. That version of the Toyota RAV4 represents 25% of sales.

The Japanese brand has significant exposure to China, with that market representing 22% of its plugin sales this year. So, if by any chance Toyota gets swallowed by the downward spiral of other Japanese brands in China (Honda, we are looking at you), its overall output will be significantly reduced.

No wonder, then, that Toyota needs to reach out to its Chinese partners in order to launch its upcoming EV models, the bZ3C and the bZ3X.

As for 100% Toyota-developed new EVs? (crickets….)

GAC

Guangzhou Automobile Group Co, also known as GAC Group, is a state-owned Chinese OEM based in Guangzhou, a city of 19 million people in the Guangdong province. It was founded in 1954 and is currently the 5th largest OEM in China, with around 2 million units sold in 2023.

Despite not having a galaxy of brands, like other Chinese OEMs, GAC has a few of them under its belt:

- Trumpchi — GAC’s ICE brand, focusing on SUVs and MPVs, with a few of its models also offering PHEV versions

- Aion — mainstream BEV brand

- Hyptec — luxury sub-brand of Aion

- GAC–Hino — joint venture, where GAC owns 90% of shares — makes Hino-based commercial vehicles.

It has 50% stakes in joint ventures with Honda (GAC–Honda) and Toyota (GAC–Toyota), where it makes models from the respective Japanese OEMs.

Finally, GAC has a minority (25%) stake in Hycan, a small BEV brand born out of cooperation with NIO. But since the startup brand left Hycan, in 2022, there hasn’t been any investment in it, and the brand is expected to disappear soon.

The main brand in the plugin market is Aion, which represents 80% of the group’s plugin vehicle sales. The share it has of the OEM’s exports is marginal (1%), but it is expected to grow in 2025.

With slowing sales in 2024, due to the lack of successful new models, and a BEV focus that led GAC to lose out in the current PHEV/EREV surge in China, the OEM hopes that new models, like the revised Aion V crossover or the new Aion UT compact hatchback, will pull them back into the growth path.

Looking at the best-selling models, Aion lives on the continued success of the Aion S and Aion Y, with the sedan being responsible for 39% of the brand’s sales while the crossover represents 46% of its sales.

Mercedes

Mercedes-Benz Group AG, also known as Mercedes, or Merc to its closest friends, is one of the most famous automotive brands worldwide, making cars in one form or another since 1885.

It is headquartered in Stuttgart, Germany, and is known as one of the Three German Premium Mary’s (Audi, BMW, and Mercedes).

The OEM is made of its namesake brand and a number of sub-brands associated with it, like the sport-focused Mercedes-AMG, the high-end luxury Mercedes-Maybach, and Mercedes Vans.

On top of this, it still has a 30% stake in Daimler Truck AG, a spinoff company of its former commercial vehicle division, as well as a 50-50% joint venture with Geely, Smart, which started in 2019.

For the purpose of counting its sales volume, because Smart is now based in Ningbo, China, and is using Geely’s platforms, drivetrains, and technology, with Mercedes being only responsible for design, I have been counting these sales under the Geely umbrella.

This means that the OEM’s volume output is basically the same as the namesake brand’s output now.

Mercedes has a large lineup of EVs, both BEV and PHEV, which means that the sales of its three best-selling EV models (Mercedes EQA, EQB, and GLC PHEV) counted together represent just 40% of its total sales. Looking at the glass half full, this means that it is not dependent on the lifecycle of one particular model, but looking at the glass half empty, it means that it lacks a star player on the team.

While its exposure to the Chinese EV market is not that significant, with that market representing just 8% of Mercedes’ total PEV sales, when looking at the total number of sales, all powertrains included, things become more concerning. In 2023, over one third of all Mercedes global sales were in China, surpassing even the total number of Mercedes sold in Europe during the same period.

This sales discrepancy with regard to China (8% of EV sales vs. 33%+ of overall sales) should be one of the major items of concern for the German make, because Mercedes could lose some 25% of its total sales, or over half a million sales, in a PEV-based Chinese market. And that scenario is less than five years away….

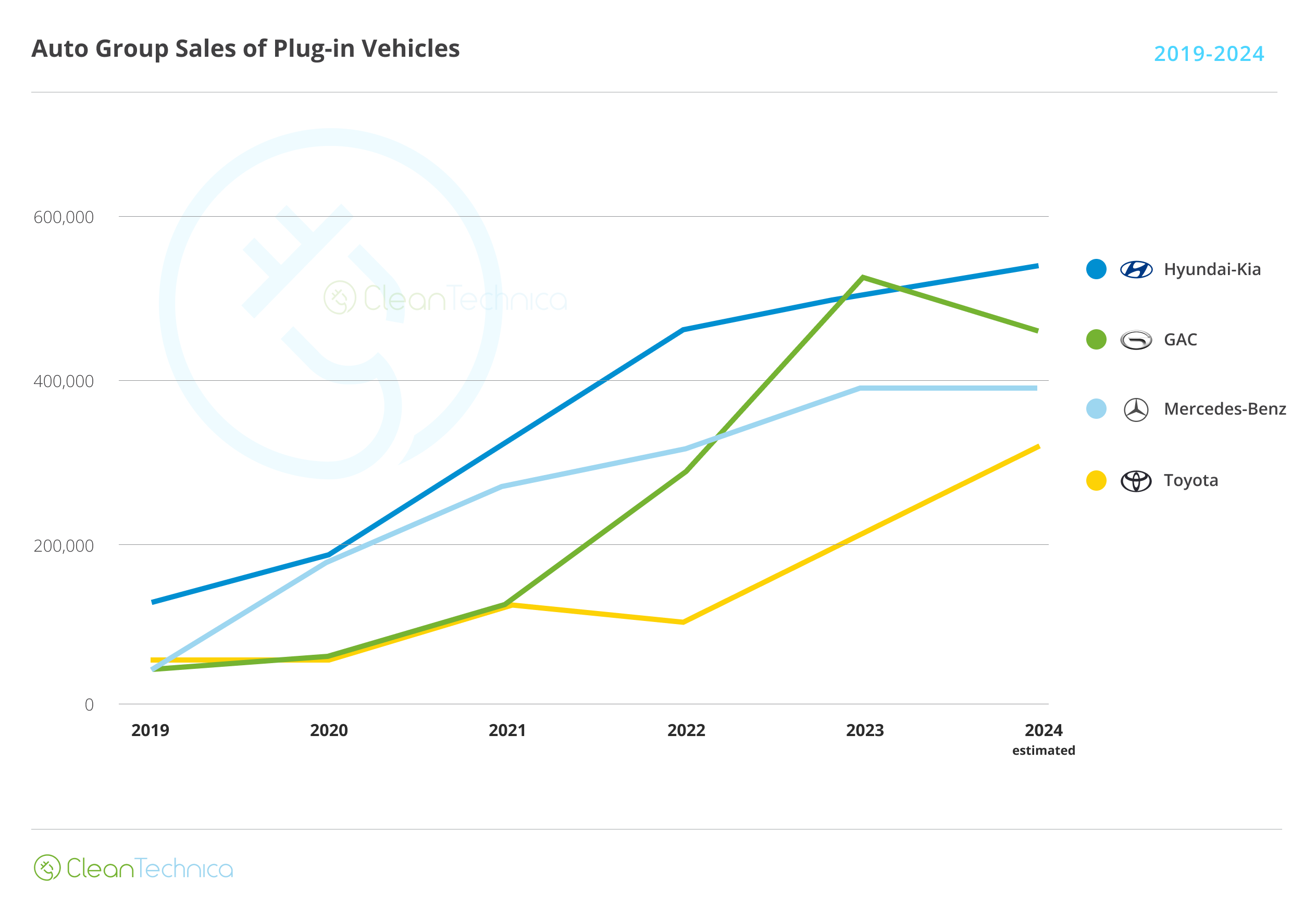

Looking at the sales of each OEM, one can see the extraordinary evolution of these OEMs in the past five years.

In fact, while the best-selling one had little more than 100,000 sales in 2019, in 2024, the lowest selling of them is expected to clock in over 300,000 units.

Looking at individual OEMs, the good work being done by Hyundai–Kia is clearly visible, with steady development over the years, and with the exception of 2023, it’s always the one with the highest volumes among these OEMs.

Given its low exposure to the Chinese market, consistent sales performances, and technological expertise, the Korean group is probably the legacy OEM that is best managing the EV transition, and I wouldn’t be surprised if it became the largest of the legacy OEMs in a PEV-based global market. And that would allow Hyundai–Kia to compete for the 4th position in a future global OEM ranking.

Mercedes was also growing consistently, until this year, so the next couple of years will be decisive for the German OEM. The much expected 2025 CLA BEV needs to land sooner than later, and it has to be a success, just like the 2026 GLC BEV, or else things can start to get messy in Stuttgart….

GAC is also in trouble, dropping sales YoY by over 50,000 units in 2024. Next year will need to see it return to growth. Hence the launch of new models and a new focus on exports. In the cut-throat Chinese market, GAC doesn’t have the scale of Geely or SAIC, let alone BYD, to be safe in the future.

Finally, Toyota. A giant in the overall market, not so much in the plugin market. Looking at the graph, while the past two years have finally seen it move the needle, that has more to do with a need to follow the electrification trend in China, where Toyota is expected to sell over 1.5 million units this year, all powertrains included, than a concerted effort to make itself noticed in the EV arena.

The Japanese OEM still has tremendous potential to be one of the main players in a PEV-based automotive market. The thing is, as years go by, the window of opportunity is starting to close, and markets where Toyota is still a major player, like China and Southeast Asia, are going EV and losing their loyalty to the Japanese OEMs, and Toyota in particular.

Unlike Hyundai–Kia, where one can see consistent deployment of new vehicles and platforms, on the Toyota side, excluding the China-only models (which are made with the help of local players), besides some average-specced PHEVs and the middle of the road bZ4X, there’s little more than plans, or concepts of a plan.

Quo Vadis, Toyota?

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy