What Is Preventing Shipping Concerns From Sailing Through The Deep & Wide Channel Of Hybridization?

It’s been a busy few weeks for me, with the Glasgow maritime decarbonization debate for Stena Teknik‘s offsite for Stena’s shipping divisions’ technical leadership, assisting a European green infrastructure investment management firm with its third €4 billion fund’s investment theses around industrial decarbonization and grid storage, assisting an Argentinian energy venture capital firm with its biofuels investment theses, and prepping for a Beijing-area executive learning session on European vs. China decarbonization pathways in a few weeks. Amazing conversations with people on multiple continents.

Anyone who reads much of what I write has probably realized that I write down and publish things as a way of processing, formalizing, and improving my thoughts and opinions. The rigor of exposing my thinking in writing forces me to make my own thinking better and more complete, and also leads to post-publication expert review. That’s a painful process for me when experts tell me that I got something clearly wrong, but it is necessary. I’m in the business of being more right sooner, not the business of pretending infallibility or protecting my ego.

Today I’ll be writing out my thoughts for the strategic pathway for maritime shipping to decarbonize. I’ve published a lot on the subject already, which is the reason Stena invited me to Scotland. But there’s an emergent strategy that makes sense to me.

This was triggered by one of my excellent conversations this week, with Elisabet Liljeblad, PhD, Stena Teknik’s Sustainability & Energy Lead. She was the person who had invited me to Glasgow, and in turn I invited her to be my guest on my Redefining Energy sub-podcast, Redefining Energy – Tech. (Insert standard podcast language here about liking and subscribing.)

Liljeblad is one of the absurdly competent, intelligent, educated, and accomplished people I’m privileged to have regular conversations with these days. Her background includes being a rifle soldier and signalist with the Swedish military in Afghanistan under the NATO ISAF mission providing security in that country, a PhD in electrophysics that had her working with NASA and ESA to measure the magnetosphere of Mercury and working with Volvo on vehicle efficiency and smart cities. Look for the podcast episodes dropping in a few weeks.

The topic of the conversation was, understandably, the various alternatives for repowering the maritime industry. I’m on record as saying that it’s going to be batteries and biodiesel, of course, but that’s the mix, not the strategic pathway.

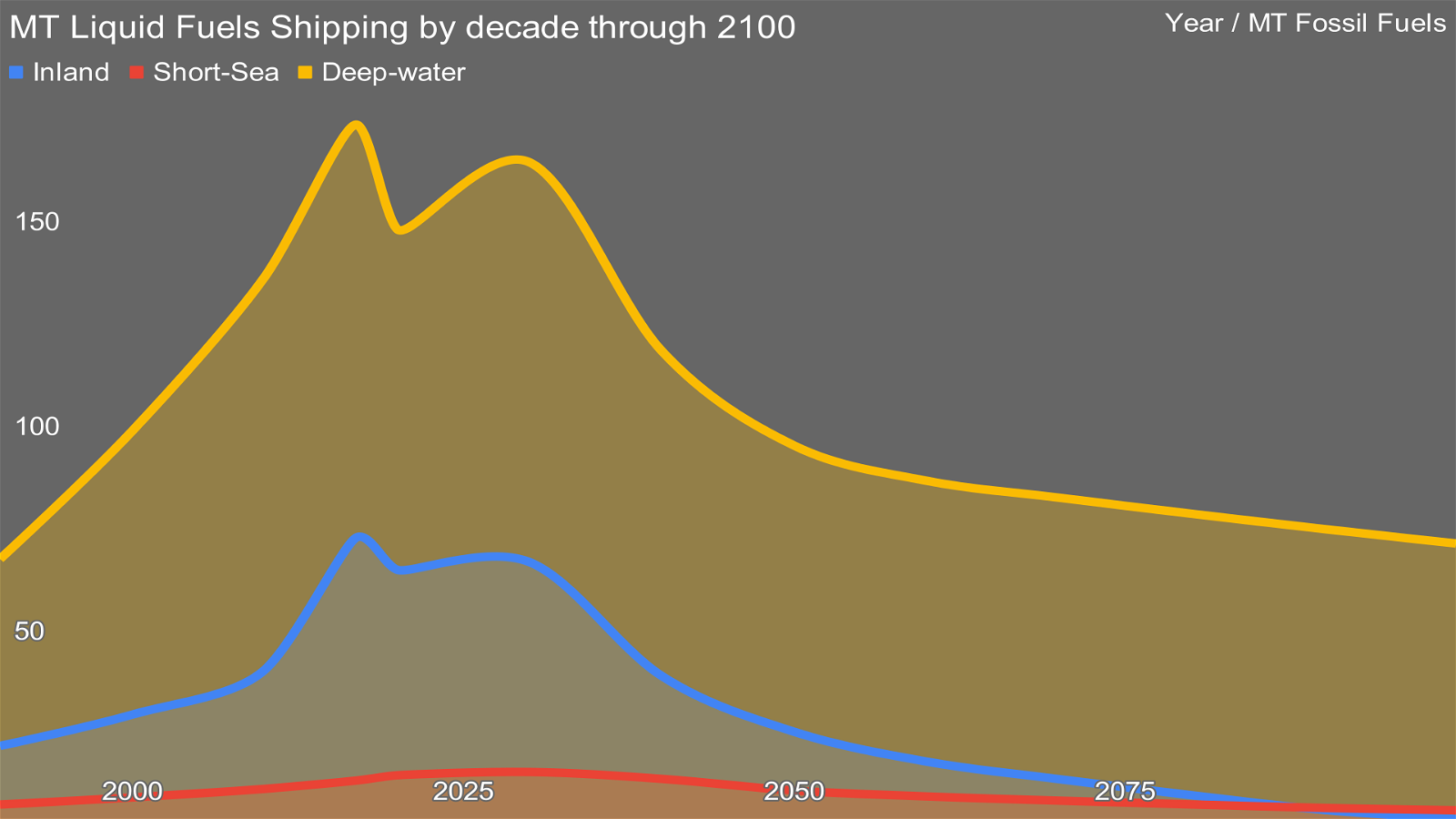

Global megatonnes of liquid fuel demand by category of shipping, chart by author

40% of bulk shipping is of coal, oil, and natural gas, and that’s mostly going away. Another 15% is raw iron ore, and that will diminish substantially with direct reduction of iron with green electricity or green hydrogen much closer to iron mines and much greater use of scrap steel in electric arc furnaces. Electrification and other efficiency measures such as slow steaming eat even further into the energy demand.

But we’re not going to be replacing the 16,000 tons of bunker fuel necessary to cross the Pacific with batteries this century, and possibly never. That’s where biodiesel will have a big play.

Liljeblad and I walked through the various options, most of which I’ve written about, sometimes extensively. Ammonia I’ve covered in portions of other articles, but never by itself as it seems so unlikely to me. I wrote about green ammonia manufacturing plans near the Suez Canal in Egypt, for example, as part of my report on the EU’s green hydrogen, vaguely colonialist plans for northern Africa. I wrote about it as part of my article on the attempts by the methanol and ammonia industries attempts to get the maritime industry pot committed to those commodities as replacements for fossil-derived bunker fuels.

Briefly, ammonia has terrible characteristics for a maritime fuel, which makes me scratch my head about any organization which isn’t manufacturing or selling the stuff today considering it. After all, it has only 42% the energy density of diesel, has to be chilled below -33° Celsius to get it into liquid form with that energy density (balmy compared to liquid hydrogen, but really?), turns into a vapor which would kill sailors in enclosed spaces like engine rooms with it, turns into a caustic gas when mixed with water which would dissolve the lungs of anyone exposed to it like the sailors, shore crews, and citizens living near ports, and then turns into a different substance which isn’t quite as harmful to human health but is still pretty bad.

Ammonia has so many strikes against it as a shipping fuel that I consider it remarkable that thoughts of it are being treated seriously. As I said to Lynn Loo, CEO and founder of the Global Centre for Maritime Decarbonization (another stunningly brilliant and accomplished person I’ve had the privilege of speaking with) a few months ago, I’m pleased that the Centre is spending millions on an ammonia bunkering pilot as it should make clear in a proven, well-funded, and transparent way that no one would want to bunker ammonia, so the floated idea can be sunk once and for all.

Liljeblad and I also spent time talking about methanol as a shipping fuel, which I consider the best of the also-rans, but still an also-ran. There are three pathways to green methanol, one of which is a great idea for decarbonizing the ~400 million tons of CO2e from current production of roughly 170 million tons of methanol globally, the next of which is deeply concerning from a climate perspective, and the last of which is scientific and economic fantasy.

The first one is diverting any anthropogenically-created biomethane from landfills, dairy barns, and the like that we can’t avoid into methanol production. As I wrote up recently, our agriculture and food waste streams are massive creators of high-global warming potential methane. While it’s naturally created and turns into carbon dioxide eventually in the atmosphere, its direct forcing is 72 times CO2 over 20 years, and 25 times CO2 over 100 years. That’s a problem, and one we have to address to get climate change under control.

Where it’s concentrated, as at landfills, sometimes it’s flared off, which turns some but not all of the methane into CO2, or used to run gas electrical generation units. After all, it’s the same stuff that’s in natural gas, just newly created instead of having been created over millions of years, so it makes electricity just fine.

For the 170 million tons of methanol, biomethane from landfills and dairy barns can be captured, and turned into a very virtuous industrial feedstock. All the methanol process does is take natural gas (or gas from coal or other fossil gases), turn it into a synthetic gas and then distill that into wood alcohol. Replacing the natural gas with biomethane that we can’t avoid creating makes a lot of sense in cleaning up a dirty industry.

If that’s what the pathway was for methanol as a maritime fuel, and that’s what the industry decided on, I’d be okay with it. But instead they would probably use anaerobic digesters to make a lot more biomethane which will leak and not be much of a solution. That’s path two.

And, of course, the fossil fuel industry would like them to make methanol from scratch from green hydrogen and CO2, because then the demand for hydrogen would be so high that blue hydrogen would be required. But making methanol molecule by molecule would be so expensive that it would be silly.

Even green methanol via captured landfill methane or anaerobic digesters is going to be 2-3 times the cost of methanol today, and it’s already up to 2.2 times as expensive as diesel per unit of energy, as I worked out recently after the head of the Methanol Institute, the global lobbing organization for the methanol industry, told me in a LinkedIn comment that I was wrong that it was more expensive. Synthetic methanol would be 2-3 times as expensive as biologically source green methanol, hence the scientific and economic fantasy.

That was in a comment related to my assessment of the stunning greenwashing that global methanol giant Methanex attempted this year. It claimed that it sailed a ship from the USA to Europe on carbon-neutral methanol. When I dug into it, I found that it had used perhaps 4% of landfill or other anthropogenically-created methane with 96% fossil-derived methane to make the methanol, and claimed the 26x global warming potential biomethane would otherwise have been released to the air, and hence made the 96% natural gas alright.

Yeah, the methanol industry isn’t sending me love notes these days.

That said, global shipping giant Maersk is committed to at least giving green methanol a go. It has contracted for 18 dual-fuel, maritime diesel- or methanol-powered ships, and will be taking delivery of the first one, a small 2,100-container vessel, from the shipyard in Ursan, South Korea, soon. That ship will be powered by actually green methanol, kind of. Dutch firm OCL Global is manufacturing the methanol from landfill methane, so it’s actually virtuous methanol. The only problem is that the landfill is in the USA, not South Korea, so the roughly 4,000 tons of green methanol required for the 21,500 kilometer journey first has to be tankered ~10,000 kilometers across the Atlantic using conventional bunker fuel. It’s greenish at best, although still better than Methanex’ claim.

Maersk claims that it will be learning a lot about powering a ship with methanol from the journey, but that’s nonsense, in my opinion. Ships powered by methanol have been puttering around since at least 2015 when Stena converted a ship to run on the stuff, although it’s not remotely green methanol. The characteristics are well known. Bunkering is understood, as methanol is transported in tankers regularly, and about 122 of ~800 ports worldwide have methanol transshipment tanks. Burning methanol in internal combustion engines is well understood. There’s not much to learn, but it is a great opportunity for Maersk to show a green win if you don’t look closely, so away it goes.

Maersk is contracting for green methanol as well, although I don’t have the same provenance as for the first maiden voyage, so can’t comment on the actual greenness of it, although I have my suspicions. But it’s worth asking, how much? Well, it ha contracted for 50,000 tons of green methanol in 2024, and more in succeeding years. I did a little math, and that looks like enough for one of the 18 ships to take five trips one-way across the Atlantic in 2024, representing perhaps 2% of the 18 ships’ fuel demand. It’s a start.

But I think it is sailing into sunk costs that won’t pay off. Methanol, as far as Liljeblad and I know, requires completely separate tanks and fuel delivery systems in ships that are set up for dual fuel capacity. That means that they have to forego some cargo capacity for the tanks, although it’s not terrible, as ships are big.

But here’s the rub, and the start of the strategic decarbonization pathway I mentioned. The other tanks will contain normal shipping fuel. And what is an increasingly normal shipping fuel? Biodiesel. As I pointed out in my assessment of the IEA’s 2023 renewables update (one where I once again and gladly suffered the slings and arrows of post-publication expert review), the world is already manufacturing 100 million tons of biofuels annually, and the large majority of those are biodiesel. HVO and HEFA — that’s hydrotreated vegetable oil biodiesel and hydrotreated esters and fatty acids biodiesel — are already bunkered globally. There are well over a million tons of the stuff burned in ships today, mostly mixed with fossil-derived fuels in various ratios.

That’s just going to increase, and as I pointed out a couple of times, concerns about displacing food with biofuels are vastly overstated and there are about ten feedstock pathways to biofuels, most of them waste from agriculture, forestry, and food production and distribution. (That’s the perspective I’m extending and qualifying for the Argentinian VC’s investment theses, by the way.) One point on that is that hydrotreating requires hydrogen, and all the hydrogen used for that today is black or gray hydrogen. It’s one of the reasons I think that biodiesel and biokerosene pathways that require hydrogen will be less economically viable over the coming decades and others will dominate.

What does this have to do with Maersk’s dual fuel methanol ships? That they’ll likely burn a lot more biodiesel in their 25- to 30-year lifespans than green methanol. Good enough, I suppose, but not exactly what is envisioned by Maersk and the methanol industry.

And now, the sensible strategy.

As I noted recently, battery energy densities are going to be jumping up by multiples in the coming years, something that’s already started. For maritime shipping, Echandia has started with lithium titanium oxide batteries which provide 40 nautical miles (74 kilometers) of range. The lithium-ion cells in Teslas, including the Semi, have three times the energy density, so the same size and weight of batteries would provide 120 nautical miles (220 kilometers) of range. CATL has started delivering and Amprius has announced lithium silicon chemistry batteries which in their first incarnations offer double the range of the lithium-ion cells, so offer 240 nautical miles (440 kilometers) of maritime range.

And lithium silicon’s maximum energy density is five times what CATL and Amprius are offering right now, and two organizations have unlocked different solutions to silicon expansion when charging, so that’s in sight commercially next decade. That promises 1,200 nautical miles or 2,200 kilometers of nautical range.

That’s a progression a smart maritime firm would bet on. Ships last 25-30 years. The batteries are going to have to be replaced every few years as they degrade somewhat and are turned into grid or behind-the-meter storage until they are recycled into new batteries. Every time a ship replaces its batteries, it doubles or triples its electric range.

And in my opinion, a lot of those batteries are going to be in shipping containers that are winched or trucked on and off ships at transshipment ports, shared with trains, and charged in the ports. Swappable batteries in shipping containers actually make sense, even though swapping batteries makes no sense for cars. That means the ship owner just gets better batteries without having to do anything every few years.

But 2,200 kilometers is next decade, and the Atlantic is 3,000 km at its narrowest point.

Consider the obvious model. Replace the 20 MW+ reciprocal engine in every ship including trans-oceanic ones in the near future with a big honking electric motor. Put as many batteries in the ship as you can in the places where you might foolishly put methanol tanks, or simply set aside and wire some hold space for containers of batteries, probably next to the plugs for freezer containers. The electric motor is about 85% to 90% efficient at turning electrons into forward motion, compared to the 50% efficiency of the reciprocal internal combustion engine burning fuel if it’s running at optimal cruising speed. Overall propulsion energy efficiency goes up for the vast majority of the trips.

Put biodiesel in increasing ratios in the fuel tanks and have a smaller, but still efficient diesel electrical generator attached to them that feeds the batteries. If your batteries get a bit low, turn on the generator to feed them, running at its optimally efficient rate.

Run only on batteries in national waters and ports, eliminating air pollution and most annoying noise.

Every two to four years sail longer trips on electrons and use the more expensive biodiesel less. Get longer range overall every few years. Now that’s a dual-fuel ship that makes sense.

And as I noted recently, the pathway for niche battery-using industries like maritime shipping is to lean heavily into the Wright’s Law-driver of cars and light trucks. Follow that massive battery manufacturing market for the maritime industry market. Don’t do something ‘special’ for ships.

So that’s the strategic pathway. Build plug-in or battery swappable hybrid ships. Get big battery range increases every few years of the vessel’s life. Run biofuels through a generator into the battery in diminishing tonnage and with increasing range. Liljeblad’s intuition and knowledge leads her to agree, but being more rigorous (as well as more intelligent) than me, she wants to run a lot of numbers before she commits to it.

Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Have a tip for CleanTechnica, want to advertise, or want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Former Tesla Battery Expert Leading Lyten Into New Lithium-Sulfur Battery Era — Podcast:

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it! We just don’t like paywalls, and so we’ve decided to ditch ours. Unfortunately, the media business is still a tough, cut-throat business with tiny margins. It’s a never-ending Olympic challenge to stay above water or even perhaps — gasp — grow. So …